The borrower may not realize that in accordance with the Federal Law “On the protection of the rights and legitimate interests of individuals when carrying out activities to repay overdue debts...” No. 230-FZ of July 3, 2016 (hereinafter referred to as Law No. 230), collectors have the right make phone calls only at certain times of the day: from 8:00 to 22:00 - during working hours, from 9:00 to 22:00 - on weekends and holidays, and no more than 2 times a day. Calling is allowed at the debtor’s place of residence and in no other cases.

The law also regulates the number of incoming calls:

- 2 times a day;

- 4 times a week;

- 16 times a month.

Consequently, if a collection agency harasses a debtor by violating the law, the debtor may not respond to such calls and may even hold him accountable.

At what time and how often can collectors call the debtor according to the law?

Russian legislation establishes strict restrictions on telephone calls from collectors, both in terms of their number and frequency. Collectors have no right to disturb citizens at night. Calls are allowed no earlier than 8 a.m. and no later than 10 p.m.

Dear readers ! To solve exactly your problem, contact our online consultant on the website. It's free. For any region.

Dear readers ! To solve exactly your problem, contact our online consultant on the website. It's free. For any region.

The law allows the following frequency of interaction between collectors and the debtor via telephone:

- per day - no more than 1 time;

- per week - no more than 2 times;

- per month - no more than 8 times.

Case resolution practice

Taking legal action against collection agencies is not uncommon.

Judicial practice regarding calls at unspecified times is ambiguous and has several options for resolving the case. In March 2021, citizen S.N. Titova appealed to the Leninsky District Court of Orenburg. with a statement of claim against Active Collection LLC demanding compensation for moral damage caused by the fact that collectors call on weekends at times not established by law (at night).

Citizen Titova S.N. she herself represented her interests in court, during the trial she was unable to prove that the calls were made at night (she did not provide the court with a printout of calls from the telephone company), which is why the court decided to dismiss the claim.

The time of calls should be taken into account at the location of the debtor. If the collector is located in a different time zone, this does not relieve him of the obligation to take into account the time of the defaulter .

In July 2021, the Khabarovsk court considered the claim of citizen M.V. Ryzhkov. to the collection agency Avanta LLC for the recovery of moral and material damages. According to the case materials, agency employees called the plaintiff at night, which caused problems with the plaintiff’s health.

Ryzhkov M.V. a doctor's report from the medical center on his state of health was provided, as well as details of calls from the cellular company. Having considered the circumstances of the case, having studied all the evidence presented, the court decided to satisfy citizen Ryzhkov’s claim in full.

Is a lawsuit with collectors or a bank inevitable? Don't despair, but start taking concrete actions. We suggest the following article is required reading - how to sue debt collectors.

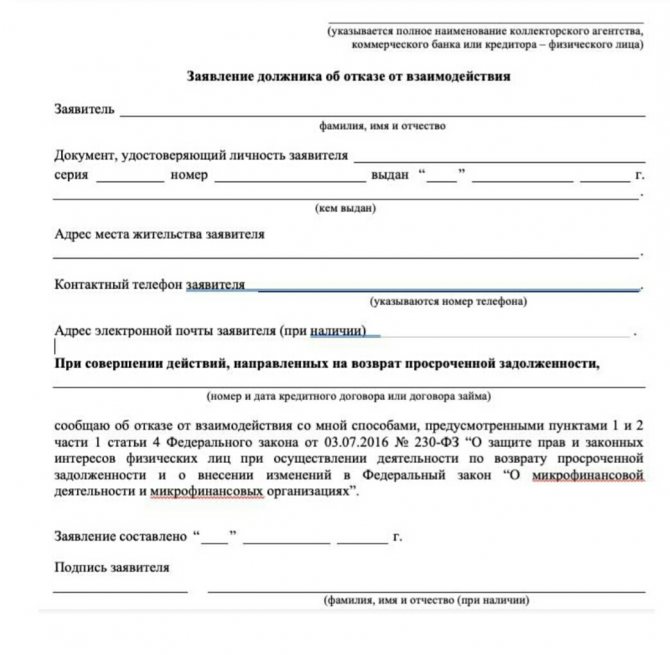

Refusal to interact with debt collectors

The debtor has the right to legally, on his own initiative, refuse to interact with debt collectors after 2 months from the date of occurrence of the collected debt.

Attention! The debtor’s right to refuse to interact with debt collectors is granted by Article 8 of Federal Law No. 230-FZ.

To do this, it is necessary to send a written notice to the creditors, drawn up in the form approved by Order of the FSSP of Russia dated January 18, 2018 No. 20.0. From the moment they receive a refusal to cooperate, collectors do not have the right to call the debtor, including on weekends.

notifications can be made by following the link: https://fssp.gov.ru/2499272/ or immediately downloading the file: prikaz_fssp_20_20191281644.doc

What other rights do collectors have?

In order to have a full understanding of his situation, the debtor should familiarize himself with the powers of such services. It is worth making a reservation and noting that bank collectors are not only intermediaries, but also internal bank services - security service, judicial departments, debt collection departments. Despite the fact that they cannot be called collectors, this does not negate their powers and obligations.

Here is the main list of rights vested in such services and structures. They can inform their opponent about the debt and name the exact amount. They can formulate requests for debt repayment, visit the borrower at home and make calls. The only thing that does not fall within the scope of their competence is making threats against clients, especially when it comes to deprivation of parental rights, inventory of property, dismissal from the workplace, or beating.

Thus, we examined from when and until when representatives of these bodies can make calls, and what rights they are endowed with. A list of obligations and restrictions on making calls was also studied. Keeping the borrower calm when receiving certain demands is the key to his own comfort and well-being.

What to do if debt collectors violate the law - where to complain

If collectors violate the law, the debtor has the right to file a claim with the head of the agency. If this measure does not bring results and the offenses continue, you should file a complaint against the debt collectors with any of the following organizations:

| Organization | Link | Possible result |

| TSB RF | https://www.cbr.ru/reception/ | Conducting inspections and applying penalties against violators |

| NAPKA | https://zhaloba.napca.ru/ | Verifying the legality of collectors’ actions and applying appropriate measures |

| Prosecutor's office | https://epp.genproc.gov.ru/web/gprf/internet-reception/personal-receptionrequest | Assistance in protecting rights in the matter of disclosure of bank secrets, personal data, as well as in the commission of an intentional crime |

| FSSP | https://fssp.gov.ru/form/ | Removal of a collection agency that violates the law from the state register |

| Rospotrebnadzor | https://rospotrebnabzor.ru/formrpn | Assistance in protecting consumer rights |

| Roskomnadzor | https://rkn.gov.ru/treatments/ask-question/ | Checking the legality of a collection agency's activities |

Time

The activities of collection agencies are regulated by the special Federal Law “On Collectors”. Article 7 of this law specifies the time when this office can make calls to the debtor:

- On a weekday, calls from the collector can be received from 8.00 to 22.00.

- On weekends - Saturday, Sunday, and holidays - calls are allowed from 9.00 to 20.00.

When agency employees call at night, early in the morning or late in the evening, a citizen has the right to appeal their actions in court, based on Article 7 of the Law “On Collectors”.

Under what circumstances can agencies send employees to the borrower?

Personal meetings do not contradict the law, and loan collection specialists can be sent to the defaulter’s home immediately after concluding an assignment agreement (debt purchase) or an agreement to provide debt collection services to the bank.

But, as a rule, in the initial stages of interaction, debt collectors call or remind you to make payments by phone or by sending SMS notifications.

If the borrower does not make contact, does not answer the phone, or is rude to the employees, they come to his home for a personal conversation.

How to communicate

IMPORTANT: the law prohibits posting information about the debtor on buildings and structures, including at the place of residence and work. In this case, you can take photographs. In addition, it is prohibited to post such information on the Internet.

Collection of other evidence

- Witness's testimonies. If the meeting is personal, then it is better to take someone with you so that in case of possible violations, he can confirm this fact in court.

- Written evidence. These include mail, notes with threats and other illegal actions.

- Other evidence. For example, this could be correspondence by email.

Currently, within the framework of the legislation, there are only some notes on provisions limiting the telephone activity of financial structures and services in relation to debtors. However, if they behave too persistently, then this fact acts as a legal basis for a citizen, in an effort to protect his own civil rights, to appeal to higher authorities to put them in their place.

The number of people with a credit burden in our country is constantly increasing. This is due to the low level of regular income in the form of income and the unavailability of some goods and services. The financial illiteracy of the population, which does not want to think and earn money, but prefers to have everything at once, also leaves its mark. As a rule, you have to pay for a long time and in large amounts, especially if we are talking about a bank loan. It’s one thing when everything is fine with money: you pay and forget.

More to read —> Tax Benefits for Disabled Persons of 3 Groups in 2021

Powers of agencies in this direction

The lower limit for when collectors can call according to the law, on weekends and various holidays, is identical to weekdays. It is evening time 22.00, and in the morning calls can only come from 9.00, i.e., in fact, it is an hour later than in the case of weekdays. That is, considering the interval in which banks can behave actively and persistently, we can note the time period from 9.00 to 22.00 on weekends (as for weekdays, this time is 8.00-22.00). A prerequisite, regardless of the day, is a local time reference.

The following actions are not allowed at the initiative of the creditor and (or) the person carrying out debt collection activities: 2) direct interaction or interaction through short text messages sent using mobile radiotelephone networks on weekdays from 10 p.m. to 8 a.m. local time time and on weekends and non-working holidays

Call rules

- The collection agency representative is required to introduce himself during the first minutes of a telephone conversation with the defaulter.

- The conversation is conducted in a civilized, polite language, without threats or psychological pressure.

- You can only call the defaulter himself. It is forbidden to bother his relatives, neighbors, and employees.

- The Law “On Collectors” determines not only the hours for telephone calls, but also the frequency. You can call no more than once a day. You can make only 2 calls in a week, and only eight in a month.

What not to do

When communicating with representatives of a collection agency, it is not recommended to:

- promise to repay the debt if you cannot do so;

- talk about existing values or savings;

- threaten, insult, fight;

- provoke visitors to aggression;

- sign documents without first reviewing or consulting a lawyer.

The conversation should take place calmly and formally. Most collection companies operate within the framework of the law, and if you show threats or physical force to an employee, the debtor himself may incur administrative or criminal liability.

Attention! There is no need to pay visitors on the spot or transfer personal property to pay off debt. Make all payments only by transferring funds to the details specified in the contract.

The legislative framework

Collectors are required to act within the framework of Federal Law No. 230 “On the protection of the rights and legitimate interests of individuals...”, which came into force at the beginning of 2021. With the adoption of this law, the requirements for the activities of collectors were tightened, and restrictions were introduced on their actions.

According to this law, employees of collection companies have the right to take any measures only if they have received a license.

A person, individual or legal entity, who has received a license to carry out collection activities is entered into the Rosreestr.

Statement of claim for compensation for moral damage.

What should relatives do?

Considering that calls to the debtor’s relatives are illegal, they have the right to use several actions to protect their rights:

- prepare a statement indicating disagreement with the processing of personal data and a request to stop such actions;

- apply for protection of your rights to the Central Bank of the Russian Federation and the prosecutor's office.

Most often you have to do both actions, since after the application the calls do not stop.

The easiest way to stop calls is to use an application that blocks such phone numbers. You can also set up a “black list”. However, this does not always bring the desired result, since calls can be made from different numbers.

If the collector uses methods of influence, for example, psychological pressure, threats, blackmail, and so on, the victim can contact the police with a statement.

However, calls are often made from unauthorized phone numbers registered to third parties, so it can be difficult to identify the real offender. The police are considering many similar cases that have no real result.

Do debt collectors sue?

Many people are concerned about whether debt collectors can sue if they do not get their money back. This argument is often used as a way to influence debtors.

Indeed, the company can appeal to a higher authority, but a person does not face a prison sentence for non-payment of a loan. The only decision that the court can make is to oblige the defaulter to repay the loan amount (for example, through monthly deductions).

Companies that have not been accredited and have not entered into an official agreement with the bank cannot apply to the highest authority.

If an appeal to the court occurs, the debtor will answer to the bank, and not to the collectors. Accordingly, there can be no talk of any repayment of exorbitant interest rates (which debt collectors often try to impose). They can only assign payment of penalties in accordance with the loan agreement.

Read also: How to find out tax debt using TIN?

You cannot sue if the statute of limitations on the loan document has expired (3 years).

Regulatory and legal framework for the activities of collectors

Previously, the activities of the debt collector were practically unrestricted, as a result of which collectors could exert psychological pressure on debtors, threaten, report debts to colleagues, relatives, etc. with impunity. Now the situation has changed somewhat: on January 1, 2021, Federal Law No. 230 dated July 3, 2016, which is aimed at protecting debtors from CAs, came into effect.

This legislative act significantly reduced the ability of the KA to obtain debts, regulating their rights in sufficient detail. The Federal Law also devotes space to the rules for calling debtors.

True, it cannot be said that the requirements of the law are implemented flawlessly (there are many cases when “debt collectors” ignore all the rules), but now citizens have a better chance of protection from illegal actions.

What they can and cannot do

To protect against illegal actions by collection professionals, debtors must know what they are entitled to and what actions are illegal.

Judicial appeal

Creditors have the right to go to court to force payment of the debt. But they do this extremely rarely, because... Litigation is lengthy and costly.

The size of the debt may not cover the legal costs, and there is also a possibility that the court will order the debt to be completely written off and the loan to be stopped.

Invitation for polite conversation

Calling and making an appointment with a client is a legal action. The conversation should be conducted politely and correctly. Insults or threats against citizens are unacceptable.

Home visit

Arriving home with the purpose of reminding about the loan and requesting payment is one of the legally established methods of interaction.

Remember that you have the right not to let strangers into your home and not to open the door for them if you do not want to communicate with them.

Come to work

Collectors have every right to visit the debtor at his place of work. However, they should not disclose personal information about the loan to colleagues.

Debt collectors can find out the whereabouts of the borrower from colleagues, and if he is at his workplace, talk to him personally.

Talk to relatives about the debt

If relatives have nothing to do with the loan, contacting them is prohibited by law.

If the borrower left the contact number of someone close to him at the time of applying for the loan, they may call him. At the same time, specialists should not disclose information about the loan. The purpose of such interaction is to find out information about the person.

Collect debts from relatives

Creditors can collect debt from a relative if he is:

- guarantor/co-borrower, i.e. bears equal responsibility with the borrower for repaying the loan;

- heir, i.e. the client died, and a loved one entered into inheritance rights, and, along with the property of the deceased, all unpaid debts pass to him.

In other cases, relatives are not responsible for the person’s obligations and do not have to pay for it.

Describe property without a court order

Only bailiffs can describe the property and sell it to repay the loan, if there is a corresponding court decision.

In addition, FSSP employees have the right to:

- enter the borrower's apartment without his consent;

- seize bank accounts;

- confiscate property.

Debt collectors do not have such powers, but they can threaten the defaulter that they will seize and seize his property in order to exert psychological pressure.

Ruin your credit history

Information about compliance with the loan payment schedule is transmitted to the credit history bureau (credit history bureau) by bank employees. If the obligations are overdue for more than a month, such information is already reflected in the credit history. No one can influence your credit history.

Attention! Sometimes representatives of a collection company promise to restore the client’s reputation with the BKI if the loan is repaid as soon as possible. This is deception and one of the methods of psychological pressure. You don't need to fall for him.

Only the borrower himself can restore his credit history by impeccably fulfilling his obligations to creditors upon subsequent receipt of loans.

Beat, be rude, threaten children

Rudeness, rudeness, threats and physical violence are prohibited by law. The collection company representative will not be able to use them when collecting debt.

If an agency employee calls you names or threatens children, contact the police and prosecutor's office. Record the conversation on a voice recorder, having previously warned the interlocutor about this. Such a recording will be direct evidence for the court.

Make a newsletter on social networks, stick notices on the door, hang up a photo of the debtor

All of the above actions constitute an invasion of privacy and may be punishable in accordance with Art. 137 of the Criminal Code of the Russian Federation. The maximum penalty for disseminating information about personal life is imprisonment for up to 4 years.

Resell debt

Changing the creditor in the agreement does not contradict the law. Collectors will be able to resell the debt to a third party under an assignment agreement. But, if none of the methods of influencing the borrower helped, and there is no property that can be described, other agencies will not want to buy such a bad debt.

If, nevertheless, the collectors resold the overdue loan, they are obliged to notify the client about the change of creditor in writing, indicating the new collection company and payment details.

Calculate interest and penalties

A change of creditor in the loan agreement should not worsen the position of the defaulter. Therefore, creditors charge penalties and fines that are provided for in the original loan agreement.

If specialists charge late fees in excess of those provided for in the loan agreement, go to court. By court decision, illegal charges will be canceled and the amount of debt reduced.

Claim a 10-year-old debt

By law, the statute of limitations for filing a claim is 3 years from the last event. It is counted from the first day of delay. When any action is taken by the creditor that can be documented, the countdown of the period is resumed.

Renewal of the term is limited to 10 years, i.e. after 10 years, the debt is automatically written off and cannot be recovered even in court.