Welcome! The topic of our meeting today is VTB 24 mortgage conditions, tariffs, programs. The increased interest in mortgages can be explained simply: for economic reasons, most Russians can only buy housing on credit. And when deciding to take out a loan, many borrowers turn to banks from the TOP-5. This choice is justified by the best conditions and security guarantees, which is important during the period of revocation of banking licenses. We will talk about the offers of VTB 24, one of the main players in the mortgage lending market. Readers will learn about the VTB 24 mortgage conditions in 2021 and the features of loan programs.

General terms

Issuing housing loans for banks involves high risks. Hence the bureaucratic barriers: requirements for the borrower, mandatory collateral insurance. VTB 24 mortgage lending conditions allow clients with a good credit rating to receive competitive rates and favorable conditions for processing applications. We will talk about the requirements for borrowers separately, but here we note a number of important general points:

- types of housing loans from VTB 24 will allow you to buy housing in new buildings and on the secondary market. Participants in government programs, holders of military certificates and family capital can use them to pay for VTB 24 mortgage loans;

- The application review procedure has been standardized. You must fill out an application form in the office or online. The application is reviewed within 4-5 days, a positive decision is valid for 122 days: during this time you need to select a property and complete the transaction. The list of documents is provided on the bank’s website; it includes the borrower’s data and information about the mortgaged property. Housing can be purchased on the territory of the Russian Federation, regardless of the place of permanent registration of the buyer;

- The initial capital in most programs is 20% of the cost of the selected object. At the same time, mortgages for the military and for a new building are issued with a 15% down payment, and loans with a 10% down payment are available for salary card holders.

These conditions do not apply to the lending program based on two documents, where the down payment is from 40%;

- Tariffs at VTB 24 bank in 2021 start at 8.4% per annum. But these are basic interest rates; the final terms of the VTB 24 mortgage are affected by the type of loan and the status of the borrower;

- The collateral property is necessarily insured for the entire mortgage period. Title and life insurance for the borrower is voluntary. VTB 24 Bank recommends taking out comprehensive insurance and offers policy owners reduced loan rates;

- it is possible to repay a mortgage loan early without additional fees and payments by calling the call center;

- mortgage bonus: customers who have taken out a mortgage have access to consumer loans at 10.9% per annum.

- Amount – minimum loan amount from 600,000 rubles to 60 million rubles.

- Currency is only rubles. There are no foreign currency mortgages at VTB 24.

- Duration – up to 30 years.

On November 24, 2017, interest rates on the main mortgage programs of VTB 24 were reduced. Now you can purchase an apartment in a new building and in a secondary building from 8.4%, if you take out a mortgage from VTB 24 partners and for an apartment of 65 sq.m.

Stages of purchasing real estate with a VTB mortgage

Stage 1: choosing a mortgage program

First, you need to determine which program you meet all the requirements for. This step will help you save quite a large amount of money on interest.

Recommended article: Mortgage and purchase and sale agreement in Rosselkhozbank

In addition to interest, the mortgage program depends on:

- Amount of down payment;

- Interest rate amount;

- Minimum income for application approval;

- Requirements for the future borrower.

Step 2: Submitting a Mortgage Application

On the official VTB website, the client should familiarize himself with all the requirements mandatory for obtaining a mortgage.

Filling out the questionnaire will not take much time, but you will have to wait much longer for a response. On average, an application is processed within 7 working days. But if you previously applied for a loan from VTB, following all the rules of the agreement, the bank will send a response in 3-4 days. Sometimes it happens that the bank responds within 1.5 months, but this happens extremely rarely.

The bank does not voice why it refuses applications; to understand the reasons for making such a decision, read the article: “Reasons for refusing a mortgage: what should borrowers take into account?”

Stage 3: property search

Upon receipt of approval for your application, the bank will indicate the amount of money you can count on. An approved loan application is valid for exactly 60 days - the period during which you need to find housing. If the requirement is not met, this application becomes invalid.

Some difficulties may arise if you are focused on secondary real estate. Most sellers are afraid to sell their home with a mortgage and refuse the deal right away. To avoid such a situation, familiarize the owner with the instructions for selling real estate through mortgage lending. Difficulties lie in wait not for the seller, but for the buyer. Since the borrower needs to choose a specific apartment that will meet all the bank’s requirements.

Stage 4: assessing the living space

The most important stage in buying a home is an independent specialist assessment of its market value. Using the data received, VTB will decide whether the property is suitable for a mortgage or not.

Stage 5: decision by the bank

Upon receiving data on the cost of an apartment from an independent expert, the bank decides whether the property is suitable for the mortgage program or not.

Remember! The bank can check the creditworthiness of the borrower and co-borrowers at any stage of document verification before signing the loan agreement. Do not rush to apply for new loans and credit cards until the transaction and settlements have taken place

Stage 6: signing the loan agreement

Before completing the transaction, you should sign a loan agreement. After this, the agreement becomes valid, and the banking organization begins to prepare the n-amount of funds.

Stage 7: conclusion of a notarial transaction

This stage has become mandatory since June 2, 2021 in situations where the property being purchased is in shared ownership or was registered in the name of a citizen under 18 years of age. But if the seller is one adult owner, the transaction is not certified by a notary.

Stage 8: state registration

You're almost at the finish line! At this step, you are required to register the transfer of rights from the seller to the buyer with Rosreestr, so that the owner’s rights apply to the newly purchased apartment. Documents are submitted to the MFC.

Recommended article: Sale and purchase agreement with a mortgage - important points for the seller and buyer

— from the Property Buyer:

- Purchase and sale agreement (not signed in advance, only in the presence of a reception specialist) 4 copies. The terms of the purchase and sale agreement with a mortgage and the risks are discussed in detail in another article;

- Loan agreement + copy;

- Mortgage + copy;

- Receipt for payment of state duty 2000 rubles + copy;

- Extract from the assessment report (optional);

- Marriage certificate (required when purchasing as joint property) + copy.

From the seller:

- Title documents (Purchase and sale agreement, Certificate of inheritance, Court decision, Agreement on transfer of apartment into ownership of citizens);

- Legal documents (Certificate of state registration of rights, Extract from the Unified State Register of Real Estate);

- Certificate of registration (if the contract does not contain information about those registered at the time of the transaction);

- Consent of the spouse, Marriage agreement (if the seller purchased the apartment during marriage).

The transaction is completed in no more than 5 - 9 business days.

Upon registration, the borrower will receive two copies (one for VTB) of the purchase and sale agreement and an extract from the Unified State Register of Real Estate.

Stage 9: property insurance

The terms of the VTB mortgage state that the mortgaged property and the life (health) of the borrower must be insured. If the rule is not followed, VTB increases the interest rate.

Mortgage insurance – what is required?

According to the law of the Russian Federation, real estate purchased with collateral must be subject to insurance against damage or damage. In addition, the apartment is insured against fire, possible flood and other unforeseen situations. This is done so that the bank can receive a 100% guarantee of the safety of the home. Such insurance from VTB is quite expensive, but you cannot refuse it, otherwise the bank will refuse a mortgage.

Stage 10: providing the client with money to purchase the property

VTB provides payment to the seller using a letter of credit account or a safe deposit box. But in the case of purchasing living space in a new building, the bank transfers the money to the developer company by bank transfer. In any case, the money will not pass through the hands of the borrower.

You can also familiarize yourself with the general conditions for the provision of a VTB mortgage loan, as well as the terms of the purchase and sale agreement, by downloading the file General conditions for concluding a VTB mortgage transaction.

Mortgage programs

Mortgages from VTB 24 Bank are of interest to potential borrowers and owners of housing loans: along with traditional lending options, there is loan refinancing.

Let's consider the types of VTB 24 mortgages, the current conditions for 2021 :

Buying a home

A classic loan for purchasing an apartment in a new building or on the secondary market. The loan size can range from 600 thousand rubles to 60 million rubles. An initial rate of 8.4% is available to clients with salary cards and comprehensive insurance policies. For borrowers of other categories the tariff is higher.

The first payment is 20%, but for people receiving salaries on VTB 24 cards it will be 10% of the purchase price, for new buildings 15%. The mortgage can be issued for 30 years, if the age of the recipient allows it;

More meters less rate

Housing loan for the purchase of apartments with an area of 100 m2 or more. This VTB 24 mortgage is interesting due to its conditions, the base rate is only 8.6% per annum. Maximum parameters: loan size up to 60 million rubles, loan period up to 30 years.

Recipients must have a net worth of at least 20% of the value of the property and take out a comprehensive insurance policy. If premises are purchased on the secondary market, insurance is required: object, personal, title for three years. For new buildings, you need to take out personal insurance and a policy for the collateral after putting the house into operation;

Military mortgage VTB 24

In 2021, it is issued in the amount of up to 2.84 million rubles, at rates starting from 8.8% per annum. It is important to know that the loan term under this program is 14 years, but can be reduced. According to the rules of military mortgages, the age limit of the borrower must be no more than 50 years at the time of repayment of the debt to the bank.

The loan is issued subject to a down payment of 15%. This condition is not critical for most NIS participants: they can apply for a loan if they have the required amount in their personal account. But if the cost of the chosen housing exceeds the established loan amount, you will have to contribute your own funds;

Victory over formalities

VTB 24 mortgage, the terms of which will allow you to quickly receive a bank decision with a minimum of documents. By submitting an application and copies of two documents (passport and dream), you can find out the result within 24 hours. Under this program, you can get a mortgage even if you are unemployed or on maternity leave, if you know certain tricks. The rate for this type of loan is from 8.4% per annum.

The disadvantages of the program include a high down payment: it is required to pay at least 50% of the cost of the property and the minimum age of the borrower is 25 years.

Loans of up to 30 million rubles are available to residents of Moscow and St. Petersburg, and borrowers from other regions can receive loans of up to 15 million rubles. The mortgage agreement is concluded for a period of up to 20 years;

Collateral property

A program for purchasing housing that is pledged and put up for sale by the owner. Bank loan terms are quite attractive: rates from 9.4%, period up to 30 years, down payment from 20%.

But borrowers need to be prepared to resolve legal issues: former owners may live in the purchased apartments, and an eviction procedure will be required.

Refinancing

Refinancing a mortgage at VTB 24 will improve the conditions for existing loans. VTB 24 offers to refinance loans up to 30 million rubles for a period of up to 30 years. But there are restrictions: the size of the loan issued should not exceed 90% of the price of the collateral property. For clients who provide two documents for the application, the loan is approved for no more than 50% of the estimated value of the collateral.

The tariff is fixed for the entire loan term. Participants in the salary project who have taken out comprehensive insurance will receive a minimum rate of 8.8%. In the absence of a policy, the tariff will be increased by 1%, and with a simplified version of the application consideration - by another 0.5%.

The VTB 24 mortgage is discussed in more detail in its nuances in a separate post.

How to use the VTB Online system

Borrowers who have entered into an appropriate agreement with the bank can use the account.

There are 2 system options available:

- For existing clients of a banking organization who have received a mortgage.

- For clients who have submitted an application for loan refinancing.

Immediately after processing the loan, the user is transferred to a personal account for regular clients. Through the account you can monitor the status of your account and the schedule of regular payments. An additional opportunity is to send applications for new loans.

Interest rate

Current interest rates on VTB 24 mortgages are presented in the table:

| Program | Bid, % | First payment, % | Note |

| Housing under construction | 8,4 | 10 | The rate of 8.4% is valid for a down payment of 50%. If the PV is less than 20%, the rate increases by 0.7 percentage points. |

| Ready housing | 8,4 | 10 | The rate of 8.4% is valid for a down payment of 50%. If the PV is less than 20%, the rate increases by 0.7 percentage points. |

| Refinancing | 8,8 | 10 | If the ratio of the loan amount to the cost of housing is more than 80%, the loan rate will increase by 0.7 percentage points. |

| Non-targeted loans secured by existing housing | 10,9 | 50 | |

| Mortgage for the military | 8,8 | 15 | Amount 2840 tr. |

| Promotion “More meters – less rate” | 8,6 | 20 | |

| Collateral property | 9,4 | 20 | |

| Mortgage with state support | 5 | 20 | If there are several children and at least one of them was born between 01/01/2018 and 12/31/2022 inclusive. |

General requirements of the bank for the borrower

Citizens who want to get a mortgage at VTB 24 must meet the following requirements:

- Russian citizenship is not necessary, i.e. Even foreigners who legally reside in the Russian Federation can get a loan;

- good credit history;

- official employment;

- total work experience - from 1 year , in the current place - more than 3 months ;

- 50% The borrower's monthly income must be sufficient to pay the monthly mortgage payment.

The borrower confirms his income with income certificates. To increase the amount of income, VTB Bank allows you to attract up to 4 co-borrowers.

Application review period

Beginning clients are interested in how long it takes to review an application. It is not always possible to stock up on a long wait. The bank understands the desire of customers to find out the answer faster, so it does not delay processing applications. The system works quickly and smoothly. Usually a preliminary response comes in just a few minutes. And the final decision on lending can be made within 3 business days. This happens when the applicant provides information that requires careful verification.

After making a decision, the client receives an SMS phone number. Sometimes the bank simply transfers funds to the account without further notice.

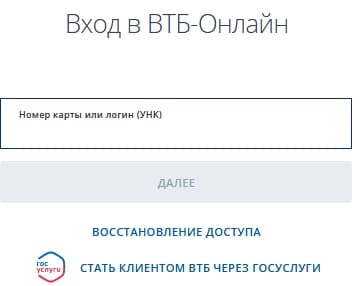

How to create a personal account

Only existing clients of the credit institution can use the remote servicing system. First of all, visit the nearest branch to conclude an agreement. Don't forget to take your ID, as the operator will refuse to serve you without it. After signing the necessary documents, you will receive a bank card. And also a sealed envelope. Inside it there are details for visiting your personal account.

This includes your password and login. You can start using the remote maintenance system right away. To do this, you need to visit the official website from a computer or other device that supports an Internet connection.

Login : https://online.vtb.ru/

You can use the VTB Bank account completely free of charge. Commission is charged only for the use of financial services:

- Transfers to individuals – 0.4% of the amount, but not less than 20 and not more than 1,000 rubles.

- Replenishment of an electronic wallet - 1.5% of the amount, but not less than 20 rubles.

- Repayment of debts in other banks - 0.8%, but not less than 20 and not more than 1,000 rubles.

- Tariffs for other services are published on the banking website.