Bank requirements for mortgage property insurance

Russian legislation gives the bank the right to determine the following conditions for insuring an apartment under a mortgage:

- risky content;

- the insurance company must be accredited by the bank;

- Compulsory insurance is carried out exclusively on structural elements.

Mortgage life insurance is completely voluntary. It protects the interests of the bank, so the credit institution is often ready to reduce the loan rate when the client issues such a policy. Typically, mortgage insurance will cost about 1% of the loan amount. At the same time, the bank is often ready to lower the rate by 1-2% if the client insures his life and health. Therefore, for the insured, such a policy can be completely free.

Which mortgage insurance should you choose?

When applying for a mortgage loan, only the collateral property must be insured. All other types of insurance: title, life, job loss, are issued at your discretion.

It is worth noting that each bank has its own insurance conditions. But, as a rule, banks insist on taking out all types of insurance. A large number of borrowers say that it is almost impossible to refuse them, since the mortgage agreement specifies sanctions that apply in case of refusal.

Mortgage insurance is not included in the cost of the loan, but is purchased separately from the insurance company. The bank can offer you its insurance partner, but you can choose absolutely any company yourself. Further, mortgage insurance will be calculated annually based on the principal amount.

Therefore, you will need to insure real estate, life, and title. And some banks require title insurance. In this case, for profitable insurance, you need to take out a comprehensive policy. The cost of such insurance does not exceed 1% of the mortgage loan.

Select insurance:

Real estate insuranceReal estate

Life InsuranceLife

Life and real estate insuranceLife and real estate

What happens if you don’t take out apartment insurance with a mortgage?

It is better to immediately become familiar with the consequences of refusing to insure collateral property. Violation of this legal requirement will result in sanctions. For example, if a Sberbank client does not obtain property insurance for a mortgage in a timely manner, then he must pay a penalty in the amount of half the annual loan rate. The fine is imposed from 31 days after the expiration of the previous insurance contract. This is much more than the cost of property insurance for a mortgage.

The bank collects the penalty from the client's account without prior notice. As a result, the borrower ends up with overdue debt, which can come as a complete surprise. In court proceedings in such cases, judges usually side with the banks. Therefore, it is better to try to resolve the issue peacefully.

How to refuse mortgage insurance?

Experts recommend resolving the issue by waiving voluntary life and health insurance, as well as title insurance (for real estate purchased on the secondary market) before signing the mortgage agreement. In this case, the procedure should be as follows:

- Study the mortgage agreement. Clarify whether the banking organization provides for a change in the interest rate if the borrower refuses the imposed types of insurance for each year of the mortgage.

- Write an application addressed to the credit manager assigned to your agreement. The application must notify you of the refusal to purchase the policy.

- Having submitted the application in two copies, it is necessary for the employee to put his signature on one of them. Thus, this will be additional confirmation that the bank has notified the borrower’s intentions.

- You should also call the Customer Support Center and try to resolve the issue promptly.

If, based on the results of all actions, the bank does not want to make concessions, then proposals from other credit institutions should be considered.

Is it possible to get money back for property insurance with a mortgage?

This possibility is provided for by current legislation. During the “cooling-off period” (14 days) from the date of issue of the policy, the client can apply for its termination and return the money paid without questions and in full. In such a situation, you will have to insure an apartment for a mortgage in another company or under another program and provide it to the bank.

After the expiration of the 14-day period, you can also cancel the policy, but in this case financial losses cannot be avoided. Some companies do not refund money at all in case of early termination of insurance when purchasing an apartment with a mortgage.

Early termination of the insurance contract is justified if, after its conclusion, the borrower found a more advantageous offer. Of course, you need to make sure that the insurer is accredited with the bank, and only after that terminate the previous contract. Otherwise, many additional difficulties will appear.

Is it possible to refuse mortgage insurance?

Most citizens perceive the insurance service as an imposed action that increases the monthly amount of payments. Therefore, many are interested in the question of how you can refuse mortgage insurance.

First, let us clarify that the refusal is issued before the main loan agreement is signed. This is completely legal, since the legislation of the Russian Federation supports the freedom of action of any citizen of the country.

Recommended article: Where is mortgage insurance cheaper?

Another case is when a loan agreement is signed with the bank, but the borrower is not notified that this service is included in it. Here you will need the help of a lawyer, as you will need to send a complaint to the consumer protection department. This paper is supported by evidence that the consumer was not aware.

The final authority is the court, where a claim is filed for a refund of funds or refusal of the loan completely. This measure is taken only in extreme cases.

What is covered by mortgage insurance?

It is mandatory to insure only structural elements! These include walls, foundation, floor, front door, windows, ceilings, stairs and roof. Interior decoration, furniture, plumbing and utilities - all this is not under financial protection. So, if flooded by neighbors, the structural elements will not be damaged. Therefore, such an event is not covered under standard mortgage property insurance.

Typically the policy covers the following risks:

- illegal actions of third parties;

- fire;

- falling objects (tree, plane);

- natural disasters;

- gas explosion.

Structural elements of apartments most often suffer from gas explosions, and houses - from fires.

General understanding of what mortgage insurance is

Mortgage insurance is a set of types of insurance that are designed to protect the financial interests of each participant in residential mortgage lending.

The need to conclude such agreements is due to the need:

- bank - in obtaining loan repayment guarantees, which allows reducing the interest rate and increasing the loan term relative to consumer loans;

- client - in obtaining financial security for the ability to fulfill their obligations in the event of death, disability, decrease in income, and other things.

The main purpose of mortgage insurance is to redistribute risks between insurers, borrowers and lenders in order to increase the reliability of the mortgage insurance system.

Types of mortgage insurance:

- insurance of property under a mortgage, which according to the agreement was pledged, against the risks of loss or damage;

- personal, which is life and disability insurance of the client (borrower or co-borrower);

- title is insurance against loss of title to collateral as a result of termination of ownership.

As an additional option, insurers offer to insure the civil liability of the premises owner against:

- by third parties during the operation of the property (for example, from cases of flooding of a neighbor’s apartment);

- by the creditor for failure to fulfill accepted financial obligations (if there is a delay, if it is impossible to make payments in the future).

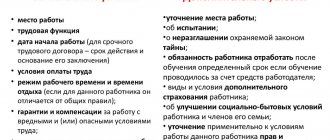

Basic terms of the mortgage insurance contract

There are standard requirements that insurance must meet. These include risk content, cases that are not insured, the procedure and timing of payments. These standards are:

- Object of insurance. Only constructive. Only elements of the building are insured; financial protection does not apply to the rest. Therefore, if an insured event occurs, the payment will be significantly less than the actual damage caused.

- Risky content. We recommend increasing the cost of insurance for an apartment with a mortgage, if it is in a new building, by adding the risk “Damage due to structural defects” to the policy. It is included in the contract for an additional fee.

- Sum insured. As a rule, it corresponds to the debt owed to the bank when signing the agreement. Some credit institutions increase it by the interest rate or 10%. The less the borrower owes the bank, the less the insured amount will be, and therefore the cost of home insurance for a mortgage.

- Cases that are not insured. These include terrorist attacks, natural wear and tear, war, disrepair, popular uprisings, and violations of safety regulations.

- Contract time. Usually 12 months. Some credit institutions require that you take out a policy for the entire period of the loan with annual payment of premiums. You need to be especially careful if the contract is concluded for a long period. In case of early repayment of the mortgage, it will be problematic for the bank to return the mortgage insurance payment made to the insurer.

Why do you need mortgage insurance?

Banks are most interested in this type of insurance. The fact is that if the borrower for some reason loses the ability to pay the loan on time, the bank suffers losses. But if you have insurance, lost income will be reimbursed.

For this reason, banks often refuse to provide a mortgage loan to those citizens who refuse to insure their lives.

What are the advantages of insurance for the borrower? Firstly, you will not lose money when third parties appear claiming ownership of the property. Secondly, in the event of disability or death, the loan will not need to be repaid to the heirs.

But mortgage insurance requires considerable costs, so many are interested in the question: how to save on mortgage insurance? We'll talk about this in more detail below.

At what stage should you take out insurance for an apartment with a mortgage?

When applying for a loan to purchase real estate, the bank already requires an insurance policy. If you plan to insure yourself directly from a credit institution, then the policy can be signed along with the mortgage agreement. You can pay for insurance services immediately at the cash desk.

Typically, the cost of mortgage insurance with another insurance company is one and a half to two times lower. It is important that it is accredited by the bank. When using the services of such companies, you can take the insurance with you along with confirmation of its payment when signing the contract. The size of the loan and the start date of the insurance agreement must match the terms and date of signing of the mortgage.

There should be no break between the completed and the new insurance contract. Banks require that before the previous insurance agreement expires, the client provides them with confirmation of payment for the next policy.

If apartment mortgage insurance was carried out for housing under construction, then immediately after putting the property into operation, you should organize its assessment, register ownership and purchase a policy. All this is provided from 2 weeks to 90 days from the date of making the corresponding entry in the Unified State Register.

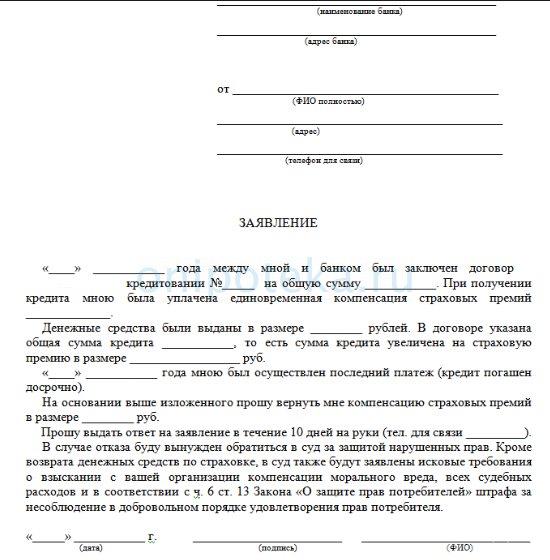

Can I get my mortgage insurance back?

Let's look at the main options for how you can get your mortgage insurance back. The condition for return is the absence of an insured event.

- After signing the loan agreement, within thirty calendar days, the citizen has the right to write a refusal and issue a refund;

- If the application from the consumer was received within 30 to 90 days after signing the contract, then the refund will be 50% of the total amount;

- Registration of a refund after full repayment of the loan is much simpler, since the encumbrance is removed from the residential premises.

- After full early repayment of the debt from the bank and provided that the possibility of return is specified in the insurance contract (policy).

Recommended article: Gazprombank mortgage insurance

To get your mortgage insurance back, you need to do a number of things:

- Contact the insurance company with a refund application; it must comply with the template established by law and must be written in duplicate. It is advisable to have a document confirming the absence of an encumbrance on the property;

- Receive a response in writing, stamped by the company, with a full expense report;

- In case of refusal, file a claim, indicating a reference to Article 958 of the Civil Code of the Russian Federation;

- Write a statement of claim to the court, attaching all available documentation on the mortgage loan.

According to judicial practice, such cases are mainly considered in favor of citizens.

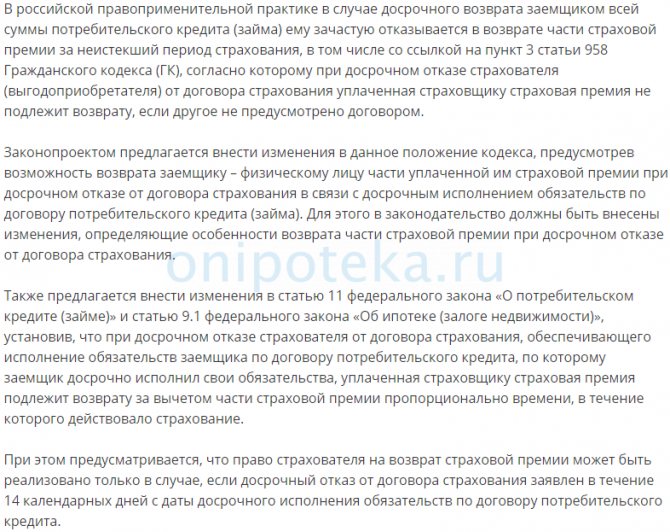

A novelty in Russian legislation may be the adoption of a number of amendments to regulations, according to which, upon full repayment of the mortgage loan, part of the insurance premium will be returned to the borrowers.

How to choose an insurance company

Although how much mortgage insurance costs is important, when choosing an insurer, it is better not to focus only on the price of its services. It is good for the company to be reliable and have a good reputation. The insurer must meet the following parameters:

- Bank accreditation . Typically, large credit institutions accept insurance protection provided only by partner companies.

- Financial indicators. You can find them out by the statistics of fees and payments. This information is freely available.

- Time on market. It is good that the insurer has been working for more than one year and has actually proven its ability to fulfill its obligations.

- Rating. It is best to buy insurance for an apartment with a mortgage from a company from the top of the TOP.

What kind of mortgage insurance is required?

Mortgage lending is a targeted loan provided to a citizen for the purchase of residential premises. The purchased property is owned by the borrower, but there is an encumbrance - a mortgage by force of law until the loan is fully repaid. Accordingly, the consumer has the right only to use it for residential purposes. According to the law, a citizen is obliged to insure the property when applying for a loan against property risks that contribute to the complete destruction of the apartment or house. This is the only type of insurance established by law that is mandatory.

A banking organization is required to provide a list of insurance companies with which it cooperates.

Let's look at what mortgage insurance is available as an additional service.

It is important to know! The bank does not have the right to base its refusal to issue a loan on the absence of a signed agreement on the provision of additional insurance options.

Credit companies offer the following types of services as an addition:

- Mortgage life insurance;

- An expanded package that includes all the main risks of non-payment of a loan or loss of property;

- Title insurance.

Recommended article: Mortgage for a room in a communal apartment or dormitory: banks, conditions, list of documents

These options are not mandatory, they are issued only at the discretion of the borrower.

Documents for obtaining insurance

Each company independently determines what documentation package is required to purchase mortgage insurance on a property. Usually it includes:

- Passport;

- Application for registration of a policy. Often executed in the form of a questionnaire requiring personal information and the condition of the property;

- Technical passport for housing;

- Contract of sale;

- Information about the loan: loan size, agreement number, interest rate, loan period, repayment schedule;

- certificate of ownership (if housing is purchased on the secondary market);

- assessment report.

How much does apartment insurance cost with a mortgage?

The final price of property insurance is influenced by various factors. The most significant are the following:

- Age of the building. It is usually possible to insure an apartment with a mortgage in a new building cheaper than in an already used building. If the building is more than 60 years old, some insurers generally refuse to provide financial protection.

- Illegal redevelopment. If redevelopment has been carried out in the apartment without prior approval from the relevant authorities, the insurer may increase the rate or refuse to sign the agreement altogether.

- Material for making walls and ceilings. The cost of home insurance for a mortgage increases significantly if wood is actively used in structural elements.

- Type of property. The price of insurance for an apartment with a mortgage is usually significantly lower than insurance for a private home.

- Presence of sources of open fire and gas. If there is a sauna, stove, fireplace or gas installed, this entails an increase in the cost of home insurance for a mortgage.

- Deterioration of the building in which the apartment is located. For houses in poor technical condition, an increasing factor is used.

- Real estate market. Insurance of new buildings is often cheaper than insurance of housing purchased on the secondary market.

So, how much does mortgage insurance cost? For apartments, the figure usually ranges from 0.1% to 0.25% of the property price. For a home, the figure can reach 0.6%.

The best solution would be comprehensive insurance. It provides complete protection. If a number of unforeseen situations arise, the insurer will be ready to make payments on the loan. For a long-term mortgage, this is a very prudent option. The main disadvantage of comprehensive insurance is high costs. They are quite logical, since the insurer takes on increased risks. As you can see, taking out a policy with comprehensive protection has its pros and cons. Everyone needs to analyze them for themselves in order to decide: to insure all or individual risks.

Compulsory and voluntary apartment insurance

The law specifies requirements regarding the mandatory registration of an insurance policy for an apartment purchased under a mortgage agreement. The client undertakes to purchase insurance with a basic package of services. Depending on the range of risks from which it protects, there are several types of insurance. Some of them are voluntary, others are mandatory.

Title insurance

The title insurance policy is voluntary and, accordingly, is issued at the discretion of the client. The presence of such a document protects the owner's property rights.

Title insurance covers the following situations:

- Judicial recognition of one of the parties to the contract as incompetent at the time of signing the papers.

- Detection of falsifications when filling out documents.

- Errors when providing information regarding living space.

- Signing documents under blackmail.

- Violations of the rights to use an apartment by persons under the age of majority or with limited legal capacity.

Financial risks in title insurance have expiration dates. The last 2 points have a statute of limitations of 3 years, the rest - 10 years.

Personal

Insurance legislation regulations do not designate the purchase of a personal insurance policy for a mortgaged apartment as mandatory. Banks have a personal interest in concluding contracts of this kind, since compensation for material compensation in the form of payments is possible.

The main risks of personal insurance are:

- death of the policyholder;

- bankruptcy of the enterprise where the policyholder works;

- registration of disability for health reasons;

- reduction or complete absence of legal capacity by the policyholder for some time due to the occurrence of a disease.

Personal insurance is issued for the entire loan period or for a short period of time (for example, 1 year). In the case of insurance for the entire period, a partial return of the premium is provided subject to premature closure of the mortgage.

What else to read:

- Apartment insurance against fire and flooding

- How to insure civil liability for apartment owners

- Concept and types of property insurance

Constructive

Insurance of a mortgaged apartment regarding the structure is mandatory. The insurance amount, which is returned if necessary, is equal to the price of the living space.

The risks stipulated by the constructive agreement are:

- robbery with theft of valuable property;

- fire (without human influence);

- collapse of part of the apartment (for example, a balcony);

- the roof is leaking, making the apartment uninhabitable.

Insurance of structural elements of an apartment for a mortgage requires a standard package of documents for all companies.

Military mortgage

The purchase of an apartment with a mortgage by military personnel is carried out under a special program. Repayment of a mortgage loan is carried out not at the expense of an individual, as is usually the case, but at the expense of the state.

In order to obtain a mortgage, a military personnel only needs to take care of opening a personal personal account. Funds will be transferred there monthly. The serviceman does not have the right to dispose of these funds at his own discretion. The maximum amount available to repay the mortgage debt in such a situation is 3 million rubles.

The program has no restrictions regarding the type of housing purchased - a serviceman can purchase either a new apartment or one that was already in use. There is a nuance to taking out insurance for property of this kind: you must sign an insurance contract annually. Only structural elements are subject to insurance.

Comprehensive insurance

The main advantage of a comprehensive insurance contract is maximum protection of all insured objects. This type of insurance is relevant for those who sign a mortgage insurance agreement for several years.

A significant disadvantage of comprehensive insurance is the cost of processing such documents. This arrangement protects the policyholder from a large number of risks, and therefore the price is appropriate.

Each policyholder decides for himself whether it is advisable to purchase a comprehensive insurance policy to protect his apartment. It must be emphasized that the client does not have the right to refuse all elements of constructive insurance.

The main question: how to make mortgage insurance cheaper?

With a little effort, you can significantly reduce your mortgage insurance rate. Some features are very simple, others require some time and effort. You can reduce the cost of apartment insurance with a mortgage as follows:

- Take advantage of promotions and special offers. Almost every insurance company from time to time holds events to attract new customers. During this period, her services are especially profitable. When insuring mortgage property, it doesn’t hurt to simply ask for a discount. Sometimes such requests are satisfied, and the cost of services is reduced by 5-10%.

- Take young co-borrowers. Insurance organizations regard the elderly as disabled. They take into account the high risks of disease and even death. This affects the percentage. Therefore, how much it costs to insure an apartment with a mortgage often depends on the age of the co-borrower.

- Transfer to another insurance company. One year after the expiration of the insurance contract, you can change the company. Some organizations offer “defectors” a discount on their services of up to 15%. Therefore, before the expiration of the current agreement, you can make inquiries about offers from other insurers.

- Register an apartment for a woman. The insurance rate when purchasing an apartment with a mortgage often depends on gender. Men usually have to pay much more than women.

- Do not buy a policy from a bank. Employees of credit institutions have a plan for selling insurance. There is no need to help them complete it. Credit institutions invest their profits in the price. Therefore, insuring mortgage property at a bank will cost many times more than directly at an insurance company.

- Find the best deal on the market. To do this, you do not need to visit the offices of all insurance companies, call them, or even go to their websites. A convenient calculator on our service will calculate how much mortgage insurance costs under specific conditions in different companies. The proposed options can be compared and the best one can be selected.

- Pay only for worthwhile risks. You shouldn’t include everything in your home mortgage insurance. Almost impossible events can be excluded. This will slightly reduce the price of insurance services.

Comparison of comprehensive and individual insurance

The bank client has the right to insure exclusively the collateral property, but insurance organizations offer a more profitable comprehensive solution. A credit institution may refuse to issue a loan or approve an application at a reduced rate to a client if he refuses to insure each item.

Note that comprehensive insurance varies within one percent of the loan size and can be reduced to 0.5%, and you can calculate the amount of mortgage insurance using the website sravni.ru. Obtaining comprehensive insurance has the following benefits: Getting one policy at a competitive rate that includes life, property and title insurance.

TOP best insurance companies in Russia for obtaining insurance for a mortgaged apartment

No. 1. Sberbank Insurance

The company is a subsidiary of Sberbank of Russia. Her specialization is insurance of bank borrowers. When it comes to mortgages, one of the best is the “Protected Borrower” program. The interest rate is affected by the gender and age of the insured. The Expert RA agency assigned Sberbank Insurance a ruAAA rating with a stable outlook.

Advantages:

- Financial stability and reliability.

- Convenience and high speed of registration in the office.

- When purchasing insurance for an apartment with a mortgage online, a 10 percent discount is provided.

Flaws:

- Inflated tariffs. The cost of insuring a property with a mortgage is higher than the market average.

- Managers are actively pushing for additional services

No. 2. Ingosstrakh

A large and well-known insurer in Russia, which has earned an impeccable reputation. In terms of market share it is in 6th place. The Expert RA agency assigned the company a ruAAA rating with a stable outlook.

The company has representative offices in many cities of the Russian Federation, including small ones. She is solvent and reliable, and does not look for formal reasons to refuse payment. The insurer offers to obtain real estate mortgage insurance online. The only thing that confuses clients is the high cost of life and health insurance policies for Sberbank, as well as many risk exclusions.

No. 3. SOGAZ

This is a large insurer that was created to insure Gazprom. The SOGAZ brand was the result of the company’s merger with VTB. As a result, the organization took the first position in terms of fees. The Expert RA agency assigned the highest rating ruAAA to the insurer with a stable outlook. The main specialization of the company is insurance of large businesses and industrial facilities. The organization does not work much with individuals. The main partner is Gazprombank.

SOGAZ has representative offices in many regions of the Russian Federation. The company is solvent and financially reliable. Disadvantages include the efforts of employees to impose voluntary insurance and the difficulty of obtaining advice or discussing issues over the telephone.

No. 4. VSK Insurance

The company is well known on the Russian market. It ranks eighth in terms of fees. Expert RA agency assigned ruAA.

VSK representative offices are open in many regions of the Russian Federation, in large and small cities. Tariffs are quite high. Users can find out how much mortgage property insurance costs and immediately apply for a policy online. Many clients note problems in getting through and communicating with a company representative by phone.

No. 5. RESO-Garantiya

Many Russians fell in love with this insurer. In terms of gross receipts, it is confidently in fourth position. The Expert RA agency assigned it a ruAA+ rating with a stable outlook. The insurer specializes in insurance of individuals; it has many positive reviews on claims settlement.

RESO-Garantiya is the only company that insures the lives of borrowers over 60 years of age. The insurer periodically conducts promotions that make it possible to insure collateral for mortgages on especially favorable terms. The somewhat unpredictable pricing is frustrating; different branches of the insurer may set different rates for one client.

No. 6. AlfaInsurance

This is a large and well-known insurer; in terms of fees it is in second position in Russia. Fitch Ratings assigned the organization a BB rating with a Positive outlook.

AlfaStrakhovanie readily provides discounts to clients who transfer from other organizations (with the exception of Sberbank borrowers). The company offers attractive rates and is financially reliable. Even if a loan is issued for a small amount, the insurer requires a medical examination.

No. 7. VTB Insurance

The company is a subsidiary of VTB. It is in 7th position in terms of fees. The Expert RA agency assigned the insurer a ruAAA rating with a stable outlook. The company operates at high rates, and VTB borrowers are insured by it. Insurance can be obtained quickly and conveniently directly from the bank. The organization is known for its high financial reliability.

The insurer offers to issue policies with a period of 3 to 20 years with a one-time payment. If the client pays off the mortgage early, the money spent on insurance will not be returned. When applying for a housing loan from VTB Bank, it is very difficult to insure yourself with another insurance company.

No. 8. Rosgosstrakh

The company is the oldest in the Russian insurance market. In the past, she was a confident leader, but in recent years she has lost her position. A blow to the reputation was dealt by the settlement of motor vehicle claims: frequent refusals and repeated underestimations of payments scare away potential clients. The company is working to change its approach to overcome the crisis.

Rosgosstrakh has a developed network of branches that operate even in small towns. Many Russians still trust her thanks to the image she has won. The company offers average rates. Since 2021, it is no longer an accredited insurer of Sberbank.

No. 9. Renaissance

The company operates in many large cities of the Russian Federation. The insurer ranks ninth in terms of fees. According to the Expert RA agency, the company meets the requirements for the ruAAA rating with a stable outlook.

The company is always open to its customers. It is easy to reach her, the operator will help you quickly carry out calculations. Since last year, it has ceased to be accredited with Sberbank.

No. 10. Zetta

Before rebranding it was called “Zurich”. It ranks 24th in terms of fees. Although the insurer is not very famous or large, it has created a positive image of customer service and fulfillment of its obligations. The Expert RA agency assigned the organization a ruA+ rating with a stable outlook.

The company is accredited with many banks and has favorable rates. Disadvantages include the need for a medical certificate for life insurance, even when the amount of mortgage insurance is small.

Why mortgage insurance might become more expensive

The final cost of mortgage insurance depends on the rates set by the insurance company. The price is influenced by factors that increase the risk of property damage or death of the borrower.

The cost of life insurance will be influenced by the following factors:

Age. The main factor in life and health insurance is the age of the borrower. The younger he is, the lower the tariff. So, the cost will differ by 5-10 times. And persons over 60 years of age may be completely denied such insurance.

Profession and working conditions. For persons who work in difficult conditions with a high risk of injury, the price will be maximum. These are, first of all, firefighters, police officers, rescuers, and so on. But for office workers the tariff will be minimal.

Health. When insuring life, you must fill out a special form indicating all diseases. You should not hide them, because in the event of disability or death, payments may be denied. Accordingly, the more serious the disease, the higher the tariff.

The cost of insurance of collateral is affected by:

Type of living space. Insuring an apartment will cost less than insuring a house.

Wall material. The cost of insuring wooden structures will be higher, since such housing is more likely to be damaged.

Year of construction. The older the house, the higher the rates.

The cost of title insurance is influenced by the following factors:

Number of transactions. If ownership of an object has been transferred many times, then the risks of third parties claiming housing increase. Therefore, the more transactions, the higher the cost of the insurance policy.

The length of time the property was held by the previous owner. This period must be at least three years, otherwise insurance will be denied or the tariff will be greatly increased.

Age of the home seller. The tariff increases because it is the elderly.

Procedure in case of an insured event

Each company determines the sequence of actions in the event of an insured event. You can find out about it from the insurance contract. The following steps are standard for most (using the example of property damage):

- Try to do everything possible to reduce or prevent damage and save the insured property.

- Without delay, call the appropriate service: • in case of flooding - housing office workers; • in case of fire – fire service; • in case of illegal actions - police officers.

- Receive documents from service representatives confirming their call and the damage caused.

- Contact the insurer so that he can arrange an inspection of the damaged property and determine the amount of damage caused.

You cannot change the picture of what happened - everything must remain in the form in which it was after the damage. If something needs to be changed to reduce damage or for safety reasons, these actions should be agreed upon with the insurance company. Without the insurer's permission, changes can be made after 2 weeks, having taken photo and video recordings in advance.

Insurance renewal

The borrower’s responsibility is to promptly renew the mortgage property insurance contract. Breaks between insurance policies are excluded.

For each day of delay, a penalty or penalty will be charged. However, in some banks, for example, in Sberbank, the penalty will begin to be calculated from the 31st day from the date of violation. During this time, you need to have time to renew your insurance policy.

Renewal is possible both with the previously selected company and with a new insurer. The main thing is that it is accredited by your bank.

What documents to provide to the insurer

The insurer may require the following documents:

- original notice of the occurrence of an insured event;

- application for insurance compensation;

- copy of the policy;

- documents from competent authorities. They must have the signature of officials and be certified by a seal. These could be: - a certificate from the Federal Hydrometeorological Service about a natural disaster - a resolution to initiate/refuse to initiate a criminal case in the State Fire Service indicating the location and cause of the fire; — certificate of illegal actions with a decision to initiate/refuse to initiate a criminal case; — a certificate of water damage describing the causes of the incident and identifying the persons responsible.

- copy of civil passport;

- a copy of the purchase and sale agreements, a copy of the Certificate of Title or other document that would confirm the insurable interest.