Organizational property tax

Chapter 30 of the Tax Code of the Russian Federation is devoted to property tax; you can familiarize yourself with it by downloading the Tax Code of the Russian Federation from our website.

This tax is regional. This type of tax also includes transport taxes, the specifics of its calculation can be read here. Taxpayers are organizations. The assets subject to taxation are fixed assets that are listed on the balance sheet of the enterprise. (Here I would like to note that land plots should not be included in this property, since they are subject to another tax - land tax.)

The tax period is a calendar year.

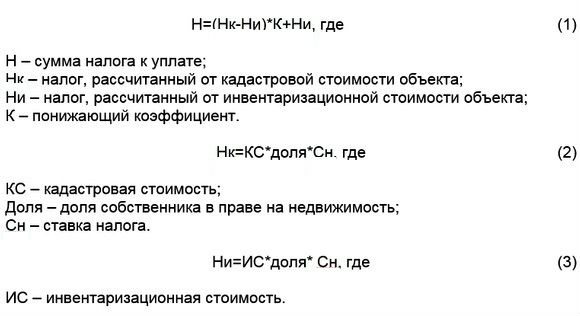

General formula for calculating property taxes for individuals in 2018

The general formula for calculating tax collection in 2021 is:

If you know all the indicators, you can calculate the amount of tax.

Important: if the region has not switched to a new taxation system, then the tax will be calculated based on the inventory value of the object.

You can read more about the calculation procedure. There will also be an example there.

Formula for calculating corporate property tax

Tax = tax base * tax rate / 100%.

The tax base for corporate property tax is the average annual residual value of these fixed assets.

On a note! In 2015, changes are expected in the calculation of property tax for individuals; you can familiarize yourself with the innovations at this link.

It should be noted that starting from 2014, some changes are being made to the calculation of property taxes: for a number of real estate objects, the tax base will be taken not from the average annual value, but from the cadastral value. Read more about this in this article.

What is residual value? This is the difference between the original cost of the property and the accrued depreciation.

How to calculate the average annual residual value?

For this purpose, the accountant takes data on the residual value of existing fixed assets on the first day of each month and the last day of December and determines the average value. Let's look at this issue using an example:

The organization has two fixed assets on its balance sheet - a car and a computer. Moreover, the computer was purchased in the summer. Monthly depreciation for a computer is 1,000 rubles, for a car – 10,000 rubles.

We determine the residual value of these assets in each month of the year, the results are summarized in the table below:

| OS name | 01.01 | 01.02 | 01.03 | 01.04 | 01.05 | 01.06 | 01.07 | 01.08 | 01.09 | 01.10 | 01.11 | 01.12 | 31.12 |

| Computer | 50000 | 49000 | 48000 | 47000 | 46000 | 45000 | 44000 | ||||||

| Automobile | 300000 | 290000 | 280000 | 270000 | 260000 | 250000 | 240000 | 230000 | 220000 | 210000 | 200000 | 190000 | 180000 |

| Total residual value | 300000 | 290000 | 280000 | 270000 | 260000 | 250000 | 290000 | 279000 | 268000 | 257000 | 246000 | 235000 | 224000 |

Next, we determine the average annual residual value as the sum of the total values in each month divided by 13.

Average annual residual value = (300,000 + 290,000 + 280,000 + 270,000 + 260,000 + 250,000 + 290,000 + 279,000 + 268,000 + 257,000 + 246,000 + 235,000 + 224,000) / 13 = 265,308 rubles .

We will calculate property tax from this figure.

Features of tax payment

Article No. 382 of the Tax Code of the Russian Federation states that for various organizations such a form of payment is provided as repayment of advance payments. If you calculate the tax amount, it will be equal to the difference in certain indicators, for the calculation of which a general formula is taken.

When calculating the advance payment, it is necessary to take into account that this indicator is 1/4 of the tax rate and the price of the property in the reporting period. The payment can be calculated in several ways, the main condition being compliance with the requirements of current legislation.

Important! To correctly perform the calculation, it is recommended to draw up a table of all residual price amounts individually for each property.

The deadline for submitting (paying) the tax is regulated by regional legislation, for example, according to the example discussed above, the enterprise must make quarterly payments, and the total amount of payments corresponds to the values specified earlier.

Conclusion

Calculating tax on property assets of legal organizations is a rather complex and labor-intensive process that takes a lot of time and requires special attention. Such calculations should only be carried out by a competent specialist so that problematic issues do not arise later.

Important! Compliance with the established procedure by law when performing property tax calculations for legal organizations. To correctly and competently perform settlement operations, it is recommended to compile summary tables, monitor, and thoroughly analyze the necessary data for calculations.

Tax rate for property tax

As for the tax rate, the peculiarity of this tax is that it is a regional tax and, accordingly, the rates are set not by the tax code, but directly by the constituent entities of the Russian Federation. But at the same time, the Tax Code of the Russian Federation stipulates that this rate cannot exceed 2.2%. As a rule, the constituent entities of the Russian Federation use this maximum rate of 2.2%.

But nevertheless, there are some regions that use lower rates.

| In our example discussed above, we determined the tax base = 265,308 rubles. Let us now directly calculate the property tax itself for a rate of 2.2%: Property tax = 265308 * 2.2% / 100% = 5837 rub. |

Regional law on property tax based on cadastral value

The possibility of paying tax at cadastral value in the region is introduced by the law of the constituent entity of the Russian Federation.

Such a law can be adopted only after approval of the results of determining the cadastral value of real estate (clause 2 of Article 372, clause 2 of Article 378.2 of the Tax Code of the Russian Federation). For example, in Moscow, the specifics of determining the tax base in relation to individual real estate objects are determined by the Moscow Law of November 5, 2003 No. 64 “On the property tax of organizations.”

If there is no law, then the calculation procedure is over for you.

Quarterly payments for corporate property tax

Also, some regions, in addition to the tax period, also introduce reporting periods on their territory (first quarter, half a year, nine months). In this case, enterprises located in this region are required to report to the tax office also on the results of each quarter and pay advance payments.

Advance payments for the quarter = average property value * tax rate / 4.

| Using the example above, let's calculate quarterly advance payments for property taxes. First quarter: Average property value = (300,000 + 290,000 + 280,000 + 270,000) / 4 = 285,000 rubles. Advance payment = (285000/4) * 2.2% / 100% = 1568 rub. Half year: Average property value = (300,000 + 290,000 + 280,000 + 270,000 + 260,000 + 250,000 + 290,000) / 7 = 277,000 rubles. Advance payment = (277000/4) * 2.2% / 100% = 1523 rub. Nine month: Average property value = (300,000 + 290,000 + 280,000 + 270,000 + 260,000 + 250,000 + 290,000 + 279,000 + 268,000 + 257,000) / 10 = 274,400 rubles. Advance payment = (274400/4) * 2.2% / 100% = 1509 rub. Year: The tax amount is calculated as shown above. Payment for the fourth quarter = tax for the year - (Advance for the first quarter + Advance for the second quarter + Advance for the third quarter) = 5837 - (1568 + 1523 + 1509) = 1237 rubles. |

How to calculate by cadastral value

To calculate the property contribution of individual real estate objects (clause 1 of Article 378.2 of the Tax Code of the Russian Federation), the cadastral value is taken from the Unified State Register of Real Estate (USRN) as of January 1 of the accounting year (Article 375 of the Tax Code of the Russian Federation).

Find out the current cadastre indicator in the territorial department of Rosreestr, on the official website of the department, or look at the Unified State Register of Real Estate (USRN) extract. If a cadastral price has not been established for a property on the regional list, do not pay the property fee. An exception is residential premises, garages, unfinished construction projects: if regional authorities have not included them in the list of objects and have not established a cadastral price, calculate the tax based on the annual average.

Calculation formula for the cadastre:

Annual ID = cadastral value × 2.2%.

If you pay an advance during the year, exclude these payments from the final payment.

If the organization did not own the property for the entire year, use the coefficient Kv in the property tax - a calculated indicator that reduces the base in proportion to the time of ownership of the property.

Kv = number of complete months of ownership / number of months in the billing period.

Let's look at an example of calculating property tax based on cadastral value in 2021 for a budget organization (similarly for commerce).

GBOU DOD SDYUSSHOR "ALLUR" owns a garage. The property is included in the regional list, its cadastral price as of 01/01/2021 is 500,000 rubles.

Annual ID = 500,000 × 2.2 = 11,000 rubles.

Deadlines for payment of corporate property tax

Deadlines for payment of payments are not provided for in the Tax Code of the Russian Federation; they are established by each subject of the Russian Federation on its territory.

However, the property tax return for the tax period must be submitted by March 30 of the year following the reporting year. For reporting periods, calculations for advance payments and declarations must be submitted by the 30th day of the month following the reporting period.

Organizational property tax: main aspects

Who should pay

Please note! Payers of property tax are legal entities that have movable or immovable property on their balance sheet as fixed assets. A complete list of property items that make up the tax base is contained in parts 1-3 of Article 374 of the Tax Code of the Russian Federation.

Based on the norms enshrined in this article, property can not only be the property of a legal entity, but also be transferred for temporary use, used on the basis of a power of attorney, received under a concession agreement, or included in joint participation.

For foreign legal entities with representative offices in Russia, the tax base consists of movable and immovable property included in the balance sheet as fixed assets, provided that this property is owned by the legal entity or received under a concession agreement.

For foreign legal entities that do not have representative offices in Russia, the tax base consists of real estate objects owned by this legal entity or received under a concession agreement.

Rates and benefits

Property tax rates are determined by the constituent entities of Russia within the limits established by Article 380 of the Tax Code of the Russian Federation. Thus, for 2016 the maximum rate is 2.2 percent. If regional authorities have not determined tax rates, apply the rates from Article 380 of the Tax Code of the Russian Federation.

There are two categories of fixed assets on which property taxes do not need to be paid. Firstly, this is preferential property (Article 381 of the Tax Code of the Russian Federation). It is excluded from the calculation of the tax base. For example, this is the property of bar associations and organizations with the status of scientific centers. Secondly, land plots and other assets that are not recognized as objects of taxation (clause 4 of article 374 of the Tax Code of the Russian Federation).

As for benefits, they can be federal (listed in Article 381 of the Tax Code of the Russian Federation) and regional. Subjects of Russia, by their laws, have the right to establish additional tax benefits and conditions for their use. Moreover, regional authorities can establish benefits similar to federal ones, but without the time limits provided for them (clause 2 of Article 372 of the Tax Code of the Russian Federation). The effect of regional benefits is limited to the territory of the corresponding constituent entity of the Russian Federation. For each category of beneficiaries, special conditions may be provided that must be met in order not to pay property tax.

How to calculate advances if there are benefits

Does the organization have preferential property? Then a special tax calculation procedure applies. The average annual cost of preferential fixed assets is calculated separately in column 4 of section 2 of the tax calculation (approved by order of the Federal Tax Service of Russia dated November 24, 2011 No. ММВ-7-11 / [email protected] ). This indicator is determined by the same rules as the average value of property to which benefits do not apply.

Organizations with benefits accrue advance payments based on the average cost using the formula:

ABpl = (Stand - St) × StN: 4,

Where

– AVpl – advance payment of property tax for the reporting period; – Cost – the average cost of property for the reporting period (excluding property, the tax base for which is determined as the cadastral value); – Сл – average cost of preferential property; – StN – tax rate.

Benefits also apply to real estate with a base in the form of cadastral value. The quarterly advance payment for “beneficiaries” is calculated using the formula:

AVpl = (Kstoim – Kneobl) × StN: 4,

Where

– AVpl – advance payment of property tax for the reporting period; – Kstoim – cadastral value of the property as of January 1 of the reporting year; – Kneobl – non-taxable cadastral value of property as of January 1 of the reporting year; – StN – tax rate.