Ksenia Filimonova, lawyer of the legal and tax consulting department of Prifinance LLC, answers:

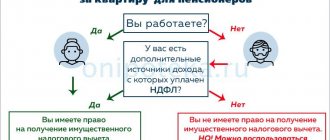

An individual has the right to receive a tax deduction of 13% in connection with the payment of interest on a mortgage.

A tax resident of the Russian Federation who is officially employed and pays personal income tax (13%) is entitled to this deduction. To understand how much tax deduction you are entitled to, you need to add up all the amounts paid for interest for all years of the mortgage loan. How to get a tax deduction on interest?

How to get a tax deduction on mortgage interest?

Since the final tax deduction cannot exceed 3 million rubles, the maximum amount you can receive is 390 thousand rubles. So what do you need to do to achieve this?

The following documents will be required:

- loan agreement with monthly repayment schedule (copy),

- purchase and sale agreement for your property (copy),

- extracts from the USRN (copy),

- transfer and acceptance certificate or agreement for participation in shared construction (copy),

- a document confirming payment of interest (this can be a certificate from a bank, receipts or bank statements),

- income certificate in form 2-NDFL, which must be obtained at the place of work.

You need to submit this entire package of documents in one of two ways.

The first option: after the end of the calendar year, submit a 3-NDFL declaration to the tax authority along with documents and a completed application for a tax refund. You can apply for a deduction after any period has passed since the purchase of real estate, but you will only be able to return the amounts that you paid during the three years preceding the filing of the declaration.

Second option: get a deduction from your employer. This means that during the year the employer will not withhold personal income tax from wages and within the amount of the tax deduction. In order to apply for a deduction in this way, you need to submit a tax application to confirm the right to deduction along with the same package of documents. After 30 days, you will receive a notification from the tax authority about the right to a property deduction, which should be submitted to your employer along with the application for the deduction.

Important! If during one calendar year you were unable to receive the full deduction amount, then the balance can be transferred to the next year. In this case, the entire procedure must be repeated.

For what years are tax refunds made on mortgage interest?

Tax refund when buying a home

How to get a tax deduction for mortgage interest over several years

In 2021, a share participation agreement was signed; a mortgage of 2,000,000 rubles was taken for the purchase for 10 years. The apartment was registered as a property in 2021. The rate was set at 11%. The size of the monthly annuity payment is equal to 27,550 rubles. Moreover, in the first months of the mortgage, about 18,000 rubles of the monthly payment are interest. With each payment, this amount gradually decreases, and payments towards the principal debt increase accordingly. Over the entire lending period, mortgage interest will amount to 1,306,000.27 rubles. That is, the buyer can return: 1,306,000.27 * 13% = 169,780.03 rubles.

With a salary of 50,000 rubles a month, you can theoretically return 78,000 in a year. But this is only theoretical. Let's assume that the salary is constant - it has not changed in the last three years and will remain constant throughout the entire term of the mortgage. In this case, at a time, a citizen can receive part of the deduction due to him for the three previous years. When the property has not yet been registered, but the mortgage has already been paid. To do this, you need to draw up three declarations in form 3-NDFL for the three previous years. And then you will have to submit a declaration annually or every three years. In this case, we do not take into account the property deduction (260 thousand) for the purchase of an apartment. Let's assume that they have already used it before and lost the right to receive it.

| Year | % in a year | 13% | Actual return |

| 2016 | 214249 | 27852 | — |

| 2017 | 200786 | 26102 | — |

| 2018 | 185764 | 24149 | — |

| 2019 | 169003 | 21970 | 78000 |

| 2020 | 150304 | 19539 | 19639 |

| 2021 | 129440 | 16827 | 16827 |

| 2022 | 106162 | 13801 | 13801 |

| 2023 | 80191 | 10424 | 10424 |

| 2024 | 51213 | 6657 | 6657 |

| 2025 | 18883 | 2454 | 2454 |

| Total | 1306000 | 169780 | 169780 |

Rights to refund of income tax arise only from the moment ownership arises. And the right of ownership arises from the moment the transfer and acceptance certificate is signed and the ownership right is registered by the relevant government bodies.

The director of the legal service “Unified Center for Protection” (edin.center) Konstantin Bobrov answers:

Mortgage interest can be refunded in the amount of 13% of the expenses that were incurred to pay mortgage interest. The maximum deduction amount cannot exceed 3 million rubles. Accordingly, you can return a sum of money in the amount of 390 thousand rubles. But the maximum amount rule applies to real estate acquired since 2014. If the property was purchased before 2014, then this restriction does not apply.

You can only receive a deduction once in your life. But you can apply for it at any time. At the same time, you can ask for its return for any period of time, but within the above maximum amount.

To register, you need to contact your employer or the tax office. The period for consideration of an application for a deduction is three months. The payment period is three to four months.

Payment is made either by crediting to a bank account, credit or debit card account, or in cash.

Instructions: how to apply for a tax deduction

How to save money if you take out a mortgage?

Get deductions for your apartment and mortgage interest at the same time

This situation is quite rare. For example, if the deadline for filing a declaration was missed. Or a shared construction project was purchased and the property arose somewhat later than the mortgage. And also the taxpayer’s income in this case must be quite large. So that the amount of personal income tax withheld for the previous 3 years covers the standard property deduction for the purchase of housing (260,000 rubles) and still remains for a deduction for mortgage interest. Typically, income taxes on the purchase of a home are refunded first, and then the interest on the mortgage.

Read more: Who issues a power of attorney on behalf of a legal entity

So, the apartment was purchased for 2 million rubles with a mortgage in 2021, the property was registered immediately. A mortgage loan was issued for 1,000,000 rubles for 10 years at 11% per annum. The size of the monthly annuity payment is equal to 13,775 rubles. RUB 9,166 of the monthly payment is interest. With each payment, this amount gradually decreases, and payments towards the body of the loan (principal debt) increase accordingly. Over the entire lending period, interest on the loan will amount to 653,000.14 rubles. With a salary of 50,000 rubles per month (600,000 per year), you can return up to 78,000 in a year. Let’s assume that the salary is constant - it has not changed in the last three years and will remain constant throughout the entire mortgage term. First, you receive a standard property deduction. Three declarations are submitted for the three years preceding the purchase of real estate.

According to declarations of 2015, 2021, 2021, we return personal income tax - 78,000 * 3 = 234,000 in 2021. We will declare the remaining 26,000 rubles towards the personal income tax refund for the purchase of real estate next year, 2021. This amount is added to the deduction for mortgage interest paid. Then every year we reimburse the remainder until the end of the loan term.

| Year | % in a year | 13,00% | Actual return |

| 2019 | 107124 | 13926 | 39926 |

| 2020 | 100393 | 13051 | 13051 |

| 2021 | 92882 | 12074 | 12074 |

| 2022 | 84501 | 10985 | 10985 |

| 2023 | 75152 | 9769 | 9769 |

| 2024 | 64720 | 8413 | 8413 |

| 2025 | 53081 | 6900 | 6900 |

| 2026 | 40095 | 5212 | 5212 |

| 2027 | 25606 | 3328 | 3328 |

| 2028 | 9441 | 1227 | 1227 |

| Total | 653000 | 84890 | 110890 |

Thus, under these conditions, during the entire term of the loan you can repay a total of: 260,000 + 84,890 = 344,890 rubles. Unless, of course, the loan is repaid for the entire planned period and is not repaid ahead of schedule. In this case, the amount of interest for using the loan can be significantly reduced. And what will be more profitable needs to be decided in each specific case.

Is it profitable to repay a loan early?

Credit organizations, relying on legislation, do not place restrictions on early repayment of mortgages. But many clients are faced with the question of whether it is advisable to partially or fully repay the debt ahead of schedule with an annuity. A simple example of calculations will allow you to answer correctly.

The initial loan parameters are 3,000,000 for 20 years at a rate of 10.5%. The overpayment for the entire period will be 4,188,335.

Let's consider several possible options. If you deposit 100,000 rubles in the first month after the start of the contract, with a decrease in the payment amount, the savings will be 126,792.33. With a decreasing period - 611,021.64.

The situation is different if repayment is made 10 years after the start of lending. With the same amount of early payment of 100,000 rubles, the savings will be 17,669.91 and 182,649.72, respectively.

Such discrepancies are associated with the technology of using annuity payments.

Important! Interest savings will be greater if repayments are made within the first few years of taking out the mortgage. It is more profitable to reduce the duration of the contract, because payment is provided for the time the money is used.

The diagrams illustrate the difference in overpayment depending on when the early repayment is made.

Read more: How to calculate the percentage of the deposit amount calculator

As for full early repayment, it will certainly also be beneficial. Thus, it certainly makes sense to pay off the debt early. But the longer it takes to get a mortgage, the smaller the savings will be.

More useful information about early repayment can be found here.

In order to make calculations based on your parameters, you can use our online calculator below.

| date | Type | Amount/rate | |

| Term | 0 months |

| Sum | 0 rub. |

| Bid | 0 % |

| Overpayment | 0 rub. |

| Start of payments | |

| End of payments | |

| Required Income |

| № | date | Payment | Main debt | Interest | Balance owed | Early repayments |

Payment methods

When you can receive compensation and how it depends on the individual’s personal desire:

- At the end of the year in which the prerogative arose. In this case, the payment will be made for the entire time and one-time from the authorized body.

- Throughout the year upon payment of interest. To do this, you will need to collect a package of documentation, write an application addressed to the boss at your place of work and receive funds. After submitting the application, the accounting department will not deduct the income tax, and it will be issued along with the salary.

To apply for a deduction, you will need to provide a list of documents. It includes standard and additional for each individual situation.

The main package includes:

- a duplicate of the applicant's identity card;

- tax return in form 3-NDFL. possible on the Internet;

- statement of income from the place of work;

- application for reimbursement;

- a copy of the personal account to which you want to transfer;

- agreement of purchase and sale or participation in shared construction;

- documents proving the fact of payment;

- extract from the unified register.

Additional documents for reimbursement of expenses will include:

- Mortgage agreement with a banking organization.

- Certificate of interest paid (issued by a credit institution).

In case of shared ownership of spouses, you will also need:

- a document that states the shares of each partner;

- duplicate of the marriage document.

An application for compensation must be submitted in any form, but with the obligatory indication of the following information:

- The header of the document contains information about the Federal Tax Service to which the petition is addressed, and the personal information of the taxpayer is also indicated here.

- The text records accurate information about the real estate object and the costs incurred.

- The application must be completed with a handwritten signature and the date of application.

ATTENTION !!! The statute of limitations for compensation of interest costs is not established at the legislative level. If an individual wishes to reimburse expenses incurred in 2021, then the application and all paperwork must be submitted from the first weekday of 2022.

Repayment options

The mortgage is issued for a fairly long period. Many borrowers want to get rid of this obligation as quickly as possible and pay off their debt ahead of schedule. This can be done in two ways:

- Increase in the monthly payment amount.

- One-time early repayment.

Read more: Free legal assistance on pension issues

In the first option, you must discuss with the bank exactly what changes this will entail. Contracts often provide for 2 options. The first of them is to reduce the loan term, the second is to reduce the monthly payment. The first one turns out to be more profitable, because in this case the interest also decreases. If a predetermined system is not provided for in the agreement, then you should contact the bank and indicate that the additional contribution is used to repay the principal debt. Thus, interest will also decrease, because it is charged only on the actual remaining debt. Another option involves paying off the mortgage in full. This is possible at any time. Some manage to collect the required amount by half the debt, while others simply pay off the last few months. It is in such a situation that it is necessary to recalculate interest. The bulk of them in most programs is included in the initial payments, which is why the overpayment has already been made in advance.

How to apply for a tax deduction - stages

There are three tax refund options in 2021:

- When visiting the inspection at your place of registration.

- When filling out the appropriate form on the Internet, you will need to go to the portal “gosuslugi.ru”.

- When submitting an application at the multifunctional center (MFC).

Tax office addresses can be found on the government services website. The user must first register. There are several stages. With simple authorization, you have limited access to submit applications and register with government agencies.

Look at the same topic: Military mortgage at VTB 24 bank - conditions, maximum amount and interest rate in [y] year

If you pass identification, an expanded range of options will be open:

- Help in finding information;

- Registration at various branches online;

- Ordering certificates via the Internet;

- Review of statistics.

To authorize you need:

- Enter the series and number of the passport;

- If your last name has changed, you must indicate the old one;

- Enter TIN details;

- Fill in the place of residence column.

It is most convenient to submit an application in electronic format. To use this type of service, you must create a personal account. You must enter taxpayer information carefully, checking the accuracy of the data.

After the site administration verifies the accuracy of the information provided, the client will have access to new services. You will be able to fill out a tax return.

When contacting the MFC, it does not matter at all which specific department you decide to contact. They are not tied to areas, so it is not necessary to come to the authority located at your place of residence.

Maximum amount

To calculate the amount required by law, you need to understand how mortgage taxes are deducted. When you start calculating funds, you need to try to take into account many restrictions that complicate the client’s position. Sometimes, due to ignorance of certain details, the user does not receive the 13 percent he is entitled to on the purchase of a home.

The state sets a maximum tax deduction threshold. It cannot be higher than 2 million rubles for the cost of housing and 3 million rubles for the interest paid by the borrower. 13 percent of these amounts will be 260,000 rubles and 390,000. The maximum refund will be 650,000 rubles. The consumer will not be able to receive more than the specified amount, no matter how expensive his apartment is.

The state will not be able to pay you more than 650,000 rubles, but it can easily pay you less. If the client earned a million and bought an apartment for 500,000 rubles, then the deduction will be the same, and 13% of it will be 65,000 rubles.

Thus, the required 130,000 of half a million over 24 months. If you register shared ownership, the amount will be distributed based on the shares assigned to each participant in the process.

Look at the same topic: How much does it cost to check the legal purity of an apartment before buying it? Is it possible to check the apartment yourself before buying?

When spouses purchase an apartment as joint property, they write a corresponding statement indicating their parts. Based on the completed documents, the amount of tax deduction for the husband and wife will be calculated. The share can be up to 10% to 90%. If one participant involved has already received a property return, then the second one will not be paid more than 50%.